Two new actions set rules for community investing, guidance for climate risk

On October 24, 2023, a trio of federal agencies issued two actions aimed at pushing the nation’s banks – especially the largest banks – to invest in underserved communities and factor climate risk into their decisions.

Although the agencies did not incorporate everything environmental groups asked for, these actions are positive steps that will help provide a much-needed course correction for financial institutions that, so far, have been driving headlong into the twin crises of climate disaster and extreme inequality.

First, the agencies issued a final rule updating the 1978 Community Reinvestment Act (CRA), a landmark law designed to address systemic inequities in access to credit though redlining, or underinvestment in low-income neighborhoods and communities of color.

The new rule encourages banks to expand access to credit, investment, and banking services in low- to moderate-income communities, supports Minority Depository Institutions and Community Development Financial Institutions, extends reporting requirements to cover online banking, and expands eligible projects to include disaster preparedness and weather resiliency.

The agencies also issued final guidance urging banks with more than $100 billion in assets to incorporate measures of climate risk into their business planning.

The Principles for Climate-Related Finance Risk Management include both physical risks, such as the harm to people and property from climate-related disasters, and transition risk, such as shifts in policy, consumer preferences, or new technologies in the shift to a lower-carbon economy.

“We should not wait for a disaster to strike before we act,” said Michael Hsu, acting comptroller of the currency. “Prudence demands we act as risks emerge.”

The two actions were approved at the October 24, 2023, meeting of the board of directors for the Federal Deposit Insurance Corporation (FDIC) and joined by the Office of the Comptroller of the Currence and the board of governors for the Federal Reserve.

Reaction

Climate finance advocates generally see the two actions as encouraging banks to invest in climate-resiliency projects in underserved areas as well as incorporate climate risk into their own business decisions.

“The climate crisis presents risks not only to individual financial institutions, but it poses a systemic risk to the entire financial system that demands action now. With these new principles, federal banking regulators are finally laying the groundwork for a regulatory system which protects our economy from growing climate financial risks,” said Adele Shraiman, senior campaign strategist for fossil-free finance at the Sierra Club.

But advocates said the agencies did not go far enough in addressing climate-related investments and risks. Neither the CRA rule nor the climate risk principles discourage banks from investing in high-carbon industries that are driving the climate crisis.

"Regulators missed a key opportunity to mitigate climate risk and discourage financing for the polluting industries devastating the climate and our country’s most vulnerable communities,” Shraiman said.

Climate risk

The twin agency actions can be seen as two sides of the same coin. On one side of the coin, the new climate financial risk principles finally recognize climate change as a threat to financial stability.

“Physical and transition risks associated with climate change could affect households, communities, businesses, and governments – damaging property, impeding business activity, affecting income, and altering the value of assets and liabilities,” the guidance says. “These risks may be propagated throughout the economy and financial system.”

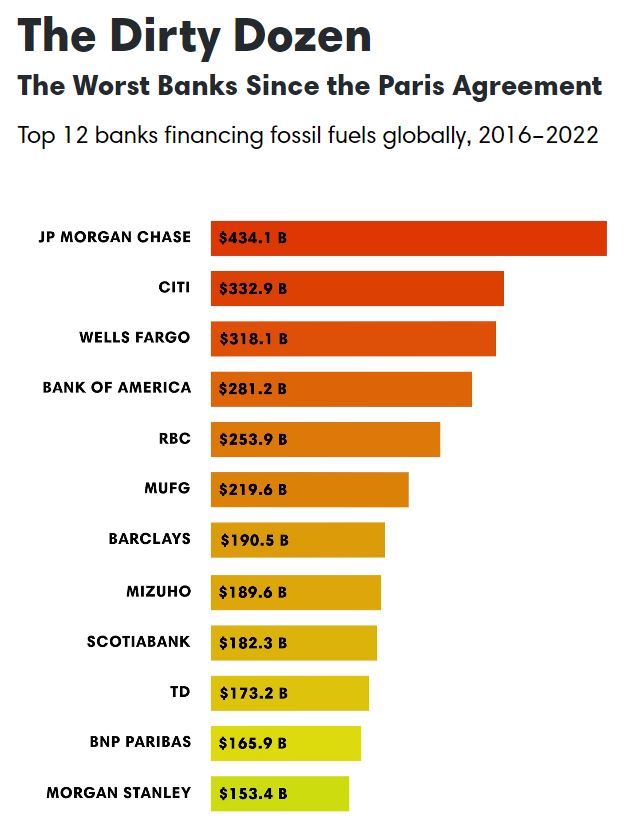

Large banks in particular have neglected to factor climate risk into their investment decisions. Since the 2015 Paris Agreement, the world’s 60 largest banks have poured $5.5 trillion into the fossil fuel industry, according to the Banking on Climate Chaos report.

About one-fourth of that amount -- $1.36 trillion – was from the world’s four largest banks – JPMorgan Chase, Citi, Wells Fargo, and Bank of America – all based in the United States.

Such large investments in fossil fuels include substantial physical and transition risk. According to the National Oceanic and Atmospheric Administration (NOAA), since 1980 the United States has experienced 372 extreme weather events with damages exceeding $1 billion each. So far in 2023 we have seen 24 climate disasters with damages exceeding $1 billion and deaths of 373 people.

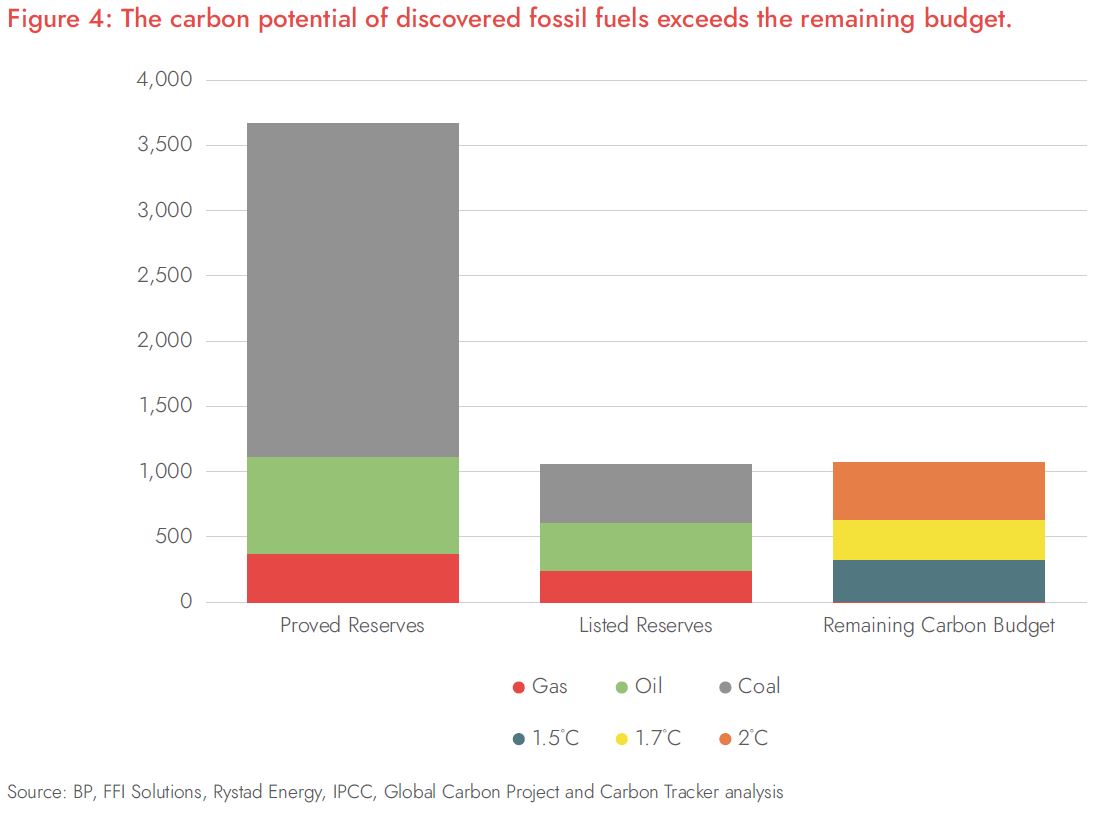

Meanwhile, 90% of known fossil fuel reserves must never be dug up and burned if we want to limit global warming to 1.5°C, according to the Unburnable Carbon report by Carbon Tracker. This means over $1 trillion of oil and gas assets risk becoming stranded in a transition to a lower carbon economy.

“Weaknesses in how a financial institution identifies, measures, monitors, and controls the physical and transition risks associated with a changing climate could adversely affect a financial institution’s safety and soundness,” the guidelines say. “The adverse effects of climate change could also include a potentially disproportionate impact on the financially vulnerable, including low-and-moderate income (LMI) and other underserved consumers and communities.”

To address this, the agencies issued a series of principles encouraging boards of directors for large banks to hold management accountable for climate risk, and encouraging management to develop processes to identify, measure, monitor, and control climate-related financial risks.

The guidelines encourage large banks to incorporate climate risk analysis into policies, procedures, and business strategy with both near and long-term planning through the use of scenario analysis. Public statements about climate-related commitments should align with internal strategies.

Community investment

On the other side of the coin, the new rule updating the Community Investment Act addresses climate risk by expanding eligible projects to include disaster preparedness and weather resiliency.

The almost 1500-page rule broadly interprets this to include projects such as:

- construction of flood control systems in a flood prone underserved urban or rural community

- retrofitting multifamily affordable housing to withstand future disasters

- promoting green space in urban areas to mitigate extreme heat

- upgrades to affordable housing such as efficient heating and air-cooling systems or more energy-efficient appliances

- community solar projects, microgrid and battery projects that could help ensure access to power to an affordable housing project in the event of severe storms

- financing community centers to serve as cooling or warming centers in low- or moderate-income areas that are more vulnerable to extreme temperatures

- assistance to small farms to adapt to drought challenges.

The new rule also addresses the rise in internet and mobile banking by requiring large banks to include geographic areas where they make significant numbers of mortgage and small business loans, whether they have a physical branch there or not, as subject to review under the Community Reinvestment Act.

The rule also allows banks to get CRA credit for any community development activities conducted with Minority Depository Institutions, Community Development Financial Institutions, Women’s Depository Institutions, and Low-Income Credit Unions.

What these actions are not

The CRA rule incentivizes banks to invest in climate resilience in communities long under-resourced through systemic inequality, and the agency guidelines encourage and incentivize banks to incorporate climate-related risk management into the everyday business practices.

But neither the guidelines nor the rule prohibit banks from investing in high carbon industries such as oil and gas – nor do they explicitly use race as a metric in community-based climate resilience.

“The principles neither prohibit nor discourage financial institutions from providing banking services to customers of any specific class or type, as permitted by law or regulation,” the climate risk guidelines say. “The decision regarding whether to make a loan or to open, close, or maintain an account rests with the financial institution.”

“The FDIC’s role with respect to climate change is centered on the financial risks that climate change may pose to the banking system and individual institutions, and the extent to which those risks impact the FDIC’s core mission and responsibilities,” said Chairman Martin Gruenberg. “The FDIC is not responsible for climate policy and does not tell banks which customers to serve.”

Although these actions do not explicitly tell big banks to stop underwriting fossil fuel projects and shift instead to community investment, they are a nudge in that direction. If these two actions motivate large banks to take a new path to a more sustainable and equitable world, they will have done their job.